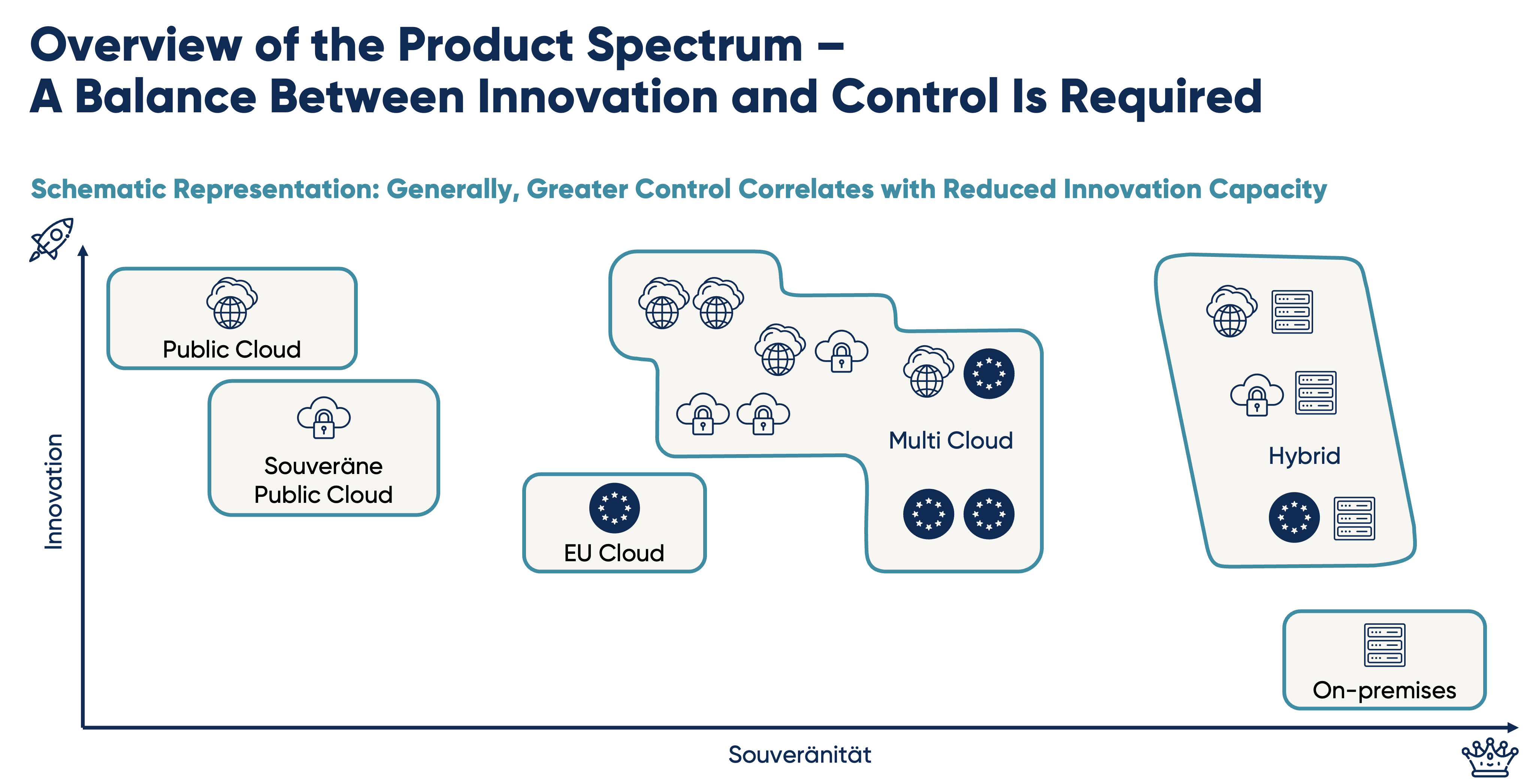

Hyperscaler Dominance: Risk or Opportunity?

The global cloud market is dominated by a few US hyperscalers. AWS, Microsoft Azure and Google Cloud control approximately 70 per cent of the worldwide cloud market – with direct implications for the strategic freedom of action of European companies.

The strong concentration on these providers poses considerable risks: the US CLOUD Act enables US authorities to access data under certain circumstances, even when stored in Europe. Standardised contractual models allow little scope for individual adaptations. High technical and financial switching barriers create vendor lock-in, and international tensions can directly threaten business continuity.

Simultaneously, hyperscalers offer continuous development of cutting-edge services and technologies (AI and analytics), attractive pricing models through global infrastructure, as well as extensive partner and developer communities.

The hyperscalers have recognised the growing demand for digital sovereignty and expanded their portfolios. AWS European Sovereign Cloud, Microsoft EU Data Boundary and Google Sovereign Cloud Portfolio offer operations in European data centres, customer-managed encryption keys, guaranteed regional data residency and legal safeguards against extraterritorial data access.

Despite these offerings, the providers remain US companies under US jurisdiction – in case of doubt, US authorities can exert pressure on parent corporations. Support, updates and security patches are delivered centrally from the United States, software remains closed source, and critical know-how resides exclusively with the providers. Moreover, sovereignty features come at a premium, and not all services are available.

The hyperscalers' sovereignty offerings are primarily compliance solutions, not genuine sovereignty guarantees. They fulfil regulatory requirements and reduce certain risks – but do not eliminate the fundamental dependency on US technology corporations.

European Alternatives – More Than Just Compliance?

Alongside the US hyperscalers, a landscape of European cloud providers (EU Cloud) has established itself, positioning themselves as sovereign alternatives.

- Established providers include STACKIT (Schwarz Digits), the cloud platform of the Schwarz Group (Lidl, Kaufland) with proven enterprise scaling, BSI partnership for the highest German security standards (Link: https://www.bsi.bund.de/DE/Service-Navi/Presse/Pressemitteilungen/Presse2025/250318_BSI_Resilienz_Cloud-Loesung.html) and exclusively European data centres.

- The Open Telekom Cloud from Deutsche Telekom offers managed cloud services by T-Systems with German legal jurisdiction, a hybrid technology base with increasingly proprietary development and long-standing enterprise experience.

- IONOS Cloud positions itself as a German cloud provider focusing on transparency and ease of use, completely European infrastructure and competitive pricing models.

- OVHcloud, the largest European cloud provider (French, publicly listed), has global infrastructure under European control and can demonstrate an important practical proof with the successful migration of critical banking workloads for Commerzbank Real.

Can European Providers Compete with the US Giants?

The answer is more nuanced than the simple dichotomy "US vs. EU" suggests. European providers offer genuine legal certainty, as they operate as EU companies under EU law, thus eliminating US CLOUD Act risk. Data protection is natively integrated – GDPR by design rather than retrospective adaptation. Furthermore, they enable greater transparency and control through direct access to decision-makers and more open communication. Local support with German-speaking teams provides deep understanding of local compliance requirements.

Simultaneously, European providers face challenges: innovation speed is slower due to smaller R&D investments in AI/ML technologies. The service portfolio is more limited with fewer managed services and specialist tools. Global reach concentrates primarily on Europe with restricted worldwide presence. The cost structure is also a reality – European providers are often more expensive than hyperscalers due to smaller scale.

![[Translate to English:]](/fileadmin/_processed_/6/9/csm_2024-05-06-PORTRAET-Rehm-Katharina_5e505aa532.jpg)

![[Translate to English:]](/fileadmin/_processed_/2/0/csm_2025-03-PORTRAIT-Christing_Maedler_dd6bd30c3f.jpg)