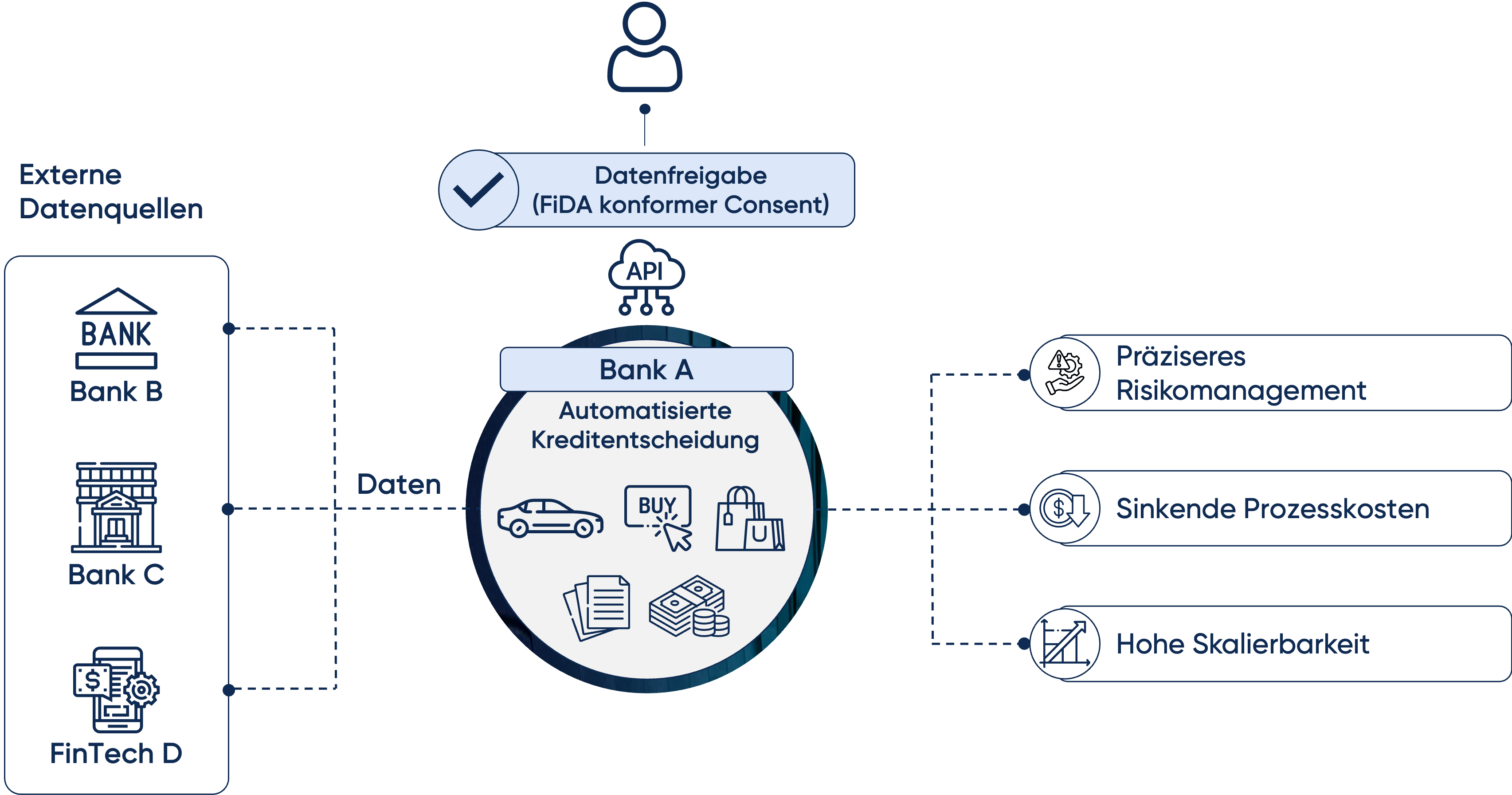

FiDA also fundamentally alters the landscape for lending. Whilst institutions are already making increasing use of disruptive technologies such as artificial intelligence to inform credit decisions, this development is taken to an entirely new level under FiDA. Banks gain access — again, exclusively upon explicit customer consent — to relevant financial data held by other institutions and service providers. This data, too, can now be systematically integrated into the credit decision process in real time for the first time.

At its core, the focus of credit assessment shifts from static metrics towards a dynamic cash flow analysis. External account transactions, recurring income, variable expenditure, existing loan and leasing obligations, as well as emerging financing models such as Buy Now Pay Later, can all be automatically incorporated into the credit model. The result is a considerably more realistic picture of a borrower's actual financial resilience.

This expanded data foundation enables a new generation of risk models:

- Finer segmentation of customer profiles

- Earlier identification of stress scenarios

- More accurate prediction of repayment probability across the full credit lifecycle

Credit decisions thus become not only faster, but also more robust. In many cases, decisions can be taken in a fully automated and near-real-time manner — a development that can significantly increase conversion rates in digital new business for institutions that adopt FiDA swiftly. At the same time, lending terms can be more individually tailored, as pricing, tenor, and collateral requirements can be aligned with the borrower's actual risk profile. This enables institutions to strengthen their competitive position whilst minimising default risk. Through the seamless integration of automated credit decisions into digital customer journeys, an institution positions itself as a reliable, data-savvy financing partner in the era of Open Finance.

![[Translate to English:]](/fileadmin/_processed_/0/6/csm_2025-03-21-PORTRAIT-Meissner-Lukas_72db6793af.jpg)

![[Translate to English:]](/fileadmin/_processed_/2/a/csm_2024-04-19-PORTRAET-Friedich-Jochen_939a81a19c.jpg)